Fixed deposit rates in Singapore are crucial for anyone looking to enhance their savings strategy. As of March 2025, these rates have seen various adjustments, with banks like DBS, UOB, and OCBC offering competitive options that can maximize your returns. When considering a fixed deposit, it is essential to understand which banks provide the best fixed deposit rates and how these can influence your financial growth. From the findings, some banks have slashed their rates, making it necessary for investors to carefully evaluate their choices and conduct a fixed deposit comparison in Singapore. Whether you are exploring 3-month deposits or 12-month plans, knowing how to choose fixed deposits effectively can lead to better financial outcomes.

In the realm of savings options, fixed deposits represent a secure way to grow your wealth. For those interested in the evolving landscape of interest rates in Singapore, particularly in March 2025, it’s clear that finding banks with high fixed deposit rates is becoming more challenging. However, understanding the various tenures and comparing fixed deposit options is vital for savvy investors. This article will discuss how to navigate this financial product, ensuring that individuals make informed decisions about their savings. As interest rates fluctuate, making the right choices about fixed deposits can result in significant benefits for your financial future.

Understanding Fixed Deposits

Fixed deposits are a popular investment option in Singapore, providing individuals with a secure way of saving money while earning interest. When you deposit a lump sum with a bank for a fixed tenure, usually ranging from a month to several years, you agree not to withdraw the funds during this period. In exchange, the bank pays you interest at a specified rate, which can significantly increase your savings over time. The importance of fixed deposits lies in their simplicity and reliability, making them ideal for conservative investors looking to preserve capital.

In Singapore, fixed deposits come with a minimum deposit requirement, often around S$10,000, depending on the bank. These deposits are attractive because the bank assures a fixed rate of return, protecting investors from market volatility. Not only do fixed deposits provide a predictable income stream, but they can also be a strategic component of a diversified portfolio, complementing riskier investments. Understanding these features is vital for anyone considering how to optimize their savings.

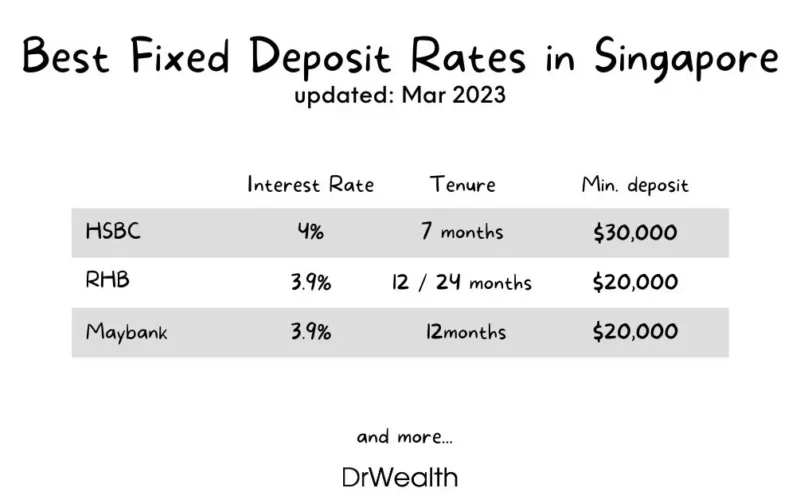

Best Fixed Deposit Rates in March 2025

As of March 2025, the landscape for fixed deposit rates in Singapore remains competitive despite a slight decline in returns across major banks. Currently, the highest 3-month fixed deposit rate is offered by the Bank of China at 2.75% per annum, while SBI leads with the best 6-month and 1-year rates at 2.85% and 2.75% respectively. These competitive rates highlight the importance of actively comparing fixed deposit offerings to ensure you secure the best returns on your investments.

Other banks, such as RHB and CIMB, provide attractive rates that may also be worth considering, especially for those looking to lock their savings for shorter tenures. With fluctuations in interest rates, it’s essential for consumers to stay informed about the latest offerings and choose banks with high fixed deposit rates to maximize their earnings. Regular checks can help identify the best fixed deposit rates and ensure your money is working as hard as it should be.

Furthermore, comparing rates across different banks can lead to better financial decisions and more significant interest earnings. Websites that offer fixed deposit comparisons in Singapore can assist in identifying which banks consistently provide the best fixed deposit rates, enabling consumers to make educated choices and plan for their financial futures effectively.

How to Choose Fixed Deposits Wisely

Choosing the right fixed deposit can be pivotal in growing your savings effectively. Firstly, assess the interest rates offered by various banks, as this will determine how much you will earn over the deposit period. Pay attention to the tenure that matches your financial goals; shorter tenures might offer lower rates, but they provide liquidity for your funds, whereas longer-term deposits might lock your money at a higher rate. Additionally, note the minimum deposit amounts, ensuring they align with your savings capacity.

It’s also essential to understand any penalties imposed on early withdrawals, as these can significantly affect your returns. Some banks may impose hefty fees if you withdraw your funds before the maturity date, negating any benefits of the interest earned. Consider these factors carefully when scrolling through options, as the best fixed deposit rates are not solely about the interest offered but also about the flexibility and terms that suit your financial situation.

Comparison of Fixed Deposit Offers from Major Banks

In Singapore, various banks provide fixed deposit options, and comparing these offers can significantly impact your savings. For instance, as of March 2025, SBI has emerged as a frontrunner with attractive rates, such as 2.85% for a 6-month tenure, making it a favored choice among savers looking for higher returns. Other notable players include the Bank of China and RHB, known for their competitive rates across different tenures, reinforcing the need for thorough comparisons to secure the best fixed deposit rates.

Additionally, consider non-financial factors such as the bank’s reputation, customer service, and the ease of accessing online banking services. A transparent and user-friendly online interface can make it easy to manage your fixed deposits and track your interest earnings. Delving deeper into fixed deposit comparisons Singapore will illuminate which banks are consistently offering the most advantageous terms and conditions.

The Importance of Fixed Deposit Rates

Understanding fixed deposit rates and their fluctuations is crucial for anyone looking to make informed financial decisions. Fixed deposit rates can be influenced by economic conditions and government policies, often reflecting broader trends in monetary policy. For instance, a decrease in T-bill yields can indicate a shift in interest rates across the banking sector, prompting banks to adjust their fixed deposit offerings. Staying aware of these trends enables investors to seize opportunities for higher returns.

Moreover, savvy investors keep an eye on historical data regarding fixed deposit rates from different banks. This analysis allows them to predict potential rate changes and strategically position their funds. By doing so, they can take advantage of the banks with high fixed deposit rates and secure a more substantial yield on their savings. Keeping abreast of fixed deposit comparisons and updates ensures you remain competitive in the evolving market.

Navigating Fixed Deposit Tenures

The tenure of a fixed deposit is a critical element to consider when selecting the right product. Depending on your financial goals, you might choose short-term deposits for liquidity or long-term ones for higher interest rates. Short-term fixed deposits typically provide flexibility, allowing you to reassess your financial position sooner without incurring heavy penalties for early withdrawal. However, these rates can be less favorable compared to long-term options.

Longer tenures can lock in higher rates, making them appealing for those who don’t need immediate access to their funds. Understanding the nuances of fixed deposit tenures can help you align your savings strategy with your financial objectives. Investing time to explore various tenures across banks can significantly benefit your overall savings strategy and returns.

The Role of Minimum Deposits in Fixed Deposits

Most banks in Singapore impose a minimum deposit amount for fixed deposits, which can significantly impact your ability to invest. This threshold varies from bank to bank, with options as low as S$500 up to S$50,000 for premium rates. Before committing to a fixed deposit, it is essential to evaluate your original investment strategy and ensure that you can comfortably meet the bank’s minimum requirements without compromising liquidity.

For those with smaller amounts to save, it may be beneficial to look into banks with promotional rates offering lower minimum deposits. These can provide an opportunity to earn interest even with limited initial investment. Keeping track of banks with lower barriers to entry while still offering competitive rates can help you maximize your returns and grow your savings effectively.

Impact of Early Withdrawals on Fixed Deposits

While fixed deposits are generally seen as a safe investment, early withdrawals can severely impact the profitability of these savings instruments. Many banks apply penalties and interest reductions, which can diminish the total returns you receive. Before committing to a fixed deposit, understanding the potential consequences of withdrawing funds prematurely is paramount to making a sound investment decision.

If you anticipate needing access to your money before the spending plan is complete, consider this risk carefully and explore alternative savings options that allow for more flexibility. Being aware of how penalties will affect your earnings will ensure your financial decisions align with your overall investment strategy.

Fixed Deposits versus Other Investment Options

When evaluating financial options, comparing fixed deposits to other investment avenues is essential. While fixed deposits offer security and guaranteed returns, investments in stocks, bonds, or mutual funds can potentially yield higher returns but come with increased risk. An investor’s risk tolerance, financial goals, and appreciation for volatility should govern this comparison.

Fixed deposits can serve as a stable component of a well-rounded investment portfolio. They provide a safety net by preserving capital that can be drawn upon in more favorable market conditions. Balancing fixed deposits with riskier investments can optimize growth while maintaining some level of security within your overall financial strategy.

Frequently Asked Questions

What are the best fixed deposit rates in Singapore for March 2025?

As of March 2025, the best fixed deposit rates in Singapore include 2.75% p.a. for a 3-month deposit offered by the Bank of China, and 2.85% p.a. for a 6-month deposit from SBI. It’s advisable to check regularly for updates as rates can change frequently.

How do I choose the best fixed deposits in Singapore?

Choosing the best fixed deposit rates in Singapore involves comparing rates from various banks, considering tenure options, and checking the minimum deposit requirements. This comparison can help you maximize your returns based on your savings goals.

Which banks offer high fixed deposit rates in Singapore?

Several banks currently offer competitive fixed deposit rates in Singapore. Some of the top ones include SBI with 2.85% for 6 months, Bank of China with 2.75% for 3 months, and RHB with 2.70% for short tenures.

What fixed deposit rates can I expect for 12 months in Singapore?

In March 2025, the best fixed deposit rates for a 12-month term in Singapore hover around 2.75% p.a. from SBI and Bank of China. It’s essential to review current offers as they may change.

How do I compare fixed deposit rates in Singapore?

To compare fixed deposit rates in Singapore effectively, look at interest rates, tenures available, and the minimum deposit amounts required by different banks. Resources like comparison websites and banks’ official pages can help streamline this process.

What should I know about fixed deposits in Singapore?

Fixed deposits are savings accounts that lock your funds for a specified period, earning a set interest rate. Early withdrawals may incur penalties, and the rates vary by bank. It’s best to stay updated on the latest fixed deposit rates to ensure optimal returns.

Are fixed deposits in Singapore affected by changes in interest rates?

Yes, fixed deposit rates in Singapore can be influenced by broader interest rate trends. For instance, recent discussions indicated that as T-bill yields dipped, many banks adjusted their fixed deposit rates accordingly in March 2025.

Is it safe to invest in fixed deposits in Singapore?

Yes, investing in fixed deposits in Singapore is generally considered safe, especially with licensed banks under the Monetary Authority of Singapore (MAS). Your deposits are insured, making them a low-risk investment.

What are the penalties for early withdrawal of fixed deposits in Singapore?

Penalties for early withdrawal of fixed deposits in Singapore vary by bank and may include forfeiting interest earnings or additional fees. Always check your bank’s terms before committing your funds.

Where can I find the latest fixed deposit rates in Singapore?

You can find the latest fixed deposit rates in Singapore on bank websites, financial comparison platforms, and financial advisories. Keeping abreast of these rates is crucial for maximizing your savings.

| Bank | Interest Rate per Annum | Tenure | Minimum Amount |

|---|---|---|---|

| SBI | 2.85% | 6 months | S$50,000 |

| SBI | 2.75% | 12 months | S$50,000 |

| Bank of China | 2.75% (mobile new placement) | 3 months | S$500 |

| Bank of China | 2.60% (mobile new placement) | 6 months | S$500 |

| Bank of China | 2.65% (mobile new placement) | 9 months | S$500 |

| RHB | 2.70% (mobile placement) | 3 months | S$20,000 |

| RHB | 2.70% (mobile placement) | 6 months | S$20,000 |

| RHB | 2.60% (mobile placement) | 12 months | S$20,000 |

| ICBC | 2.65% (mobile placement) | 3 months | S$500 |

| Hong Leong Finance | 2.60% (mobile placement) | 6 months | S$5,000 |

| CIMB | 2.55% | 3 months | S$10,000 |

| Citibank | 2.50% | 3/6 months | S$50,000 |

| OCBC | 2.45% (mobile placement) | 6 months | S$30,000 |

| Maybank | 2.45% (mobile placement) | 6 months | S$20,000 |

| DBS/POSB | 2.45% | 12 months | S$1,000 (max S$19,999) |

| UOB | 2.40% | 6 months | S$10,000 (fresh funds) |

| Standard Chartered | 2.30% | 6 months | S$25,000 |

| HSBC | 2.25% | 6 months | S$30,000 |

| HSBC | 2.10% | 3 months | S$30,000 |

Summary

Fixed Deposit Rates Singapore have seen fluctuations, particularly as of March 2025, where banks are offering competitive returns on fixed deposits. Notably, SBI leads the rates with up to 2.85% for a six-month tenure, ensuring savers can maximize their investment. As fixed deposit rates continue to adjust in response to market conditions, it’s essential for individuals to compare these options regularly to secure the best yields for their savings.