CPF retirement planning is a vital aspect of securing financial stability for Singaporeans as they approach their golden years. The Central Provident Fund (CPF) system not only provides a solid framework for retirement savings but also adapts to the evolving needs of retirees, especially with the CPF updates for 2024. Understanding the various retirement sums available, including the Basic, Full, and Enhanced Retirement Sums, is essential for individuals to ensure adequate monthly payouts. As the retirement age changes, and with new policies for self-employed CPF benefits coming into play, it becomes increasingly important to strategize effectively. Proper CPF retirement planning empowers individuals to achieve financial security for retirees, ensuring a comfortable and fulfilling lifestyle in retirement.

Retirement savings strategies in Singapore hinge on the comprehensive CPF system, which is crucial for those looking to secure their financial future. With the upcoming enhancements in the retirement sums, it’s essential for residents to familiarize themselves with how these adjustments will affect their pensions. As the government introduces changes to the retirement age and extends benefits to self-employed workers, individuals must adapt their financial planning accordingly. This proactive approach can significantly influence the quality of life for retirees, offering them peace of mind and stability. By focusing on CPF retirement planning, Singaporeans can navigate the evolving landscape of retirement savings more effectively.

Understanding CPF Retirement Planning

CPF retirement planning is crucial for Singaporean citizens seeking financial stability in their later years. The Central Provident Fund (CPF) system is structured to help individuals save systematically, allowing both employees and employers to contribute to retirement savings. This model contrasts sharply with tax-funded pensions found in many other countries, making CPF a unique feature of Singapore’s financial landscape. It’s essential for citizens to grasp the retirement sum tiers—Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS)—to make informed decisions about their long-term financial security.

The recent updates to the CPF system, particularly for 2024, emphasize the importance of planning ahead. With the increasing retirement sums, individuals must assess their current savings and contributions to ensure they can meet the new requirements. This planning not only impacts their immediate financial health but also affects their lifestyle and independence during retirement. Understanding how to navigate these changes is key to achieving a comfortable retirement.

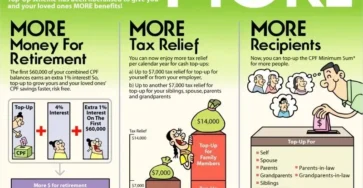

Key Updates to CPF Retirement Sums in 2024

In 2024, the Singapore government will implement significant changes to the CPF retirement sums, which are crucial for determining the monthly payouts retirees receive. For instance, the Basic Retirement Sum (BRS) will increase from SGD 96,000 to SGD 105,000, directly influencing the financial security of many retirees. These updates are designed to keep pace with rising living costs, ensuring that retirees can maintain a decent standard of living. Understanding these changes is critical for individuals nearing retirement, as they will need to adjust their savings strategies accordingly.

Moreover, the Full Retirement Sum (FRS) and Enhanced Retirement Sum (ERS) will also see increases, which means that those aiming for a more comfortable retirement need to be proactive in their savings. Retirees relying solely on CPF payouts must plan adequately to meet these new financial thresholds. These enhancements are part of the government’s ongoing commitment to ensure that all Singaporeans can enjoy financial security in their golden years.

Changes to the Retirement Age: What You Need to Know

The retirement age in Singapore is set to gradually increase, with the minimum age remaining at 63 in 2024 but rising to 64 by 2026 and 65 by 2030. This incremental approach allows workers more time in the workforce, enabling them to contribute longer to their CPF accounts. As life expectancy continues to rise, this adjustment acknowledges the reality that many individuals will need to support themselves financially for longer periods after retiring.

By increasing the retirement age, the government aims to help workers accumulate more savings in their CPF accounts. This is particularly essential for those who may not have sufficient funds saved up for retirement. It’s important for individuals to prepare for this change by considering how it fits into their overall retirement planning, including their potential CPF contributions and any additional savings they may need.

Self-Employed CPF Benefits: New Opportunities in 2024

The introduction of new CPF benefits for self-employed individuals marks a significant shift in Singapore’s retirement planning landscape. Starting in 2024, self-employed workers, including freelancers and small business owners, will have access to monthly payouts ranging from SGD 200 to SGD 400, depending on their contributions. This inclusion aims to provide these workers with financial security comparable to that of salaried employees, acknowledging the growing gig economy and the need for inclusive policies.

Additionally, self-employed individuals are encouraged to make voluntary contributions to their CPF accounts. This move not only helps them boost their retirement savings but also provides a safety net as they navigate the uncertainties of self-employment. By taking advantage of these new policies, self-employed workers can better prepare for their financial futures, ensuring they have adequate resources during their retirement years.

Future Projections for Enhanced Retirement Sum

The Enhanced Retirement Sum (ERS) is projected to increase significantly over the next few years, reaching SGD 426,000 by 2025, which will provide higher monthly payouts under the CPF LIFE scheme. This tier is crucial for those looking to maximize their retirement income and maintain a comfortable lifestyle in their golden years. Understanding these future projections allows individuals to plan strategically, ensuring they can meet the necessary savings goals to qualify for higher payouts.

As the ERS continues to rise, individuals should remain proactive in their CPF contributions. With the anticipated increases in monthly payouts, planning for retirement becomes even more critical. By staying informed about the changes and adjusting their savings strategies accordingly, Singaporeans can ensure they are well-prepared for the financial demands of retirement.

Revised Withdrawal and Transfer Policies for Retirees

In 2024, the Singapore government will revise its withdrawal and transfer policies to enhance the efficiency of the CPF system. Individuals aged 55 and above will see their funds from the Ordinary Account and Special Account automatically transferred to the Retirement Account (RA) to meet the Full Retirement Sum (FRS) limit. This ensures that retirees have a dedicated pool of savings aimed at long-term financial security, allowing them to access their funds more easily when needed.

Moreover, any excess funds in the Ordinary Account above the FRS will still be withdrawable, providing retirees with immediate financial flexibility. Starting in 2025, with the merging of the Special Account into the RA, retirees will benefit from higher long-term interest rates on their retirement savings. These policy updates are designed to maximize the growth of CPF funds, ensuring that retirees can enjoy a more secure financial future.

Preparing for Retirement: Action Steps for Singaporeans

As the CPF system evolves, it is essential for Singaporeans to take proactive steps to prepare for retirement. Maximizing CPF contributions is one of the most effective strategies individuals can adopt to ensure they meet the new retirement sums. By contributing more to their CPF accounts, they can secure higher monthly payouts, which is crucial for maintaining their quality of life in retirement.

Additionally, exploring the various CPF LIFE options can help individuals tailor their retirement plans to their specific needs. Attending CPF seminars and staying informed about policy changes will empower Singaporeans to make educated decisions regarding their financial futures. With the right planning and preparation, they can navigate the complexities of retirement and achieve the financial security they desire.

Financial Security for Retirees: The Role of CPF

The CPF system plays a vital role in ensuring financial security for retirees in Singapore. By providing a structured savings model, it allows individuals to accumulate funds throughout their working lives, which can then be accessed during retirement. With the introduction of updated retirement sums and the increased importance of retirement planning, CPF is more crucial than ever for ensuring that retirees can cover their living expenses and healthcare needs.

Furthermore, the CPF system’s flexibility in allowing withdrawals and transfers means that retirees can manage their funds according to their unique circumstances. Whether one is relying on the Basic, Full, or Enhanced Retirement Sum, having a well-structured CPF account can significantly alleviate financial stress during retirement. As Singapore continues to adapt to changing demographics and economic conditions, the role of CPF in securing financial stability for retirees will remain paramount.

Frequently Asked Questions

What are the key CPF retirement planning updates for 2024?

In 2024, significant updates to CPF retirement planning include increases in the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS). These adjustments are designed to ensure that retirees have adequate savings to meet rising living costs and enhance their financial security.

How will the changes in CPF retirement sums affect my retirement planning?

The changes in CPF retirement sums will directly impact your retirement planning by determining the amount you need to save in your CPF account to receive monthly payouts. With the new sums, retirees can expect higher monthly payouts, thus improving their financial security.

What is the new retirement age in Singapore as part of CPF updates?

The minimum retirement age in Singapore will remain at 63 in 2024, increasing incrementally to 64 in July 2026 and to 65 by 2030. This gradual increase is part of the CPF updates aimed at helping individuals contribute more to their retirement savings.

What benefits do self-employed individuals receive under the CPF retirement planning updates?

Starting in 2024, self-employed individuals can benefit from CPF retirement planning with monthly payouts ranging from SGD 200 to SGD 400, depending on their contributions. This effort aims to include self-employed workers in the CPF system and enhance their financial security during retirement.

How can I maximize my CPF retirement savings with the updated retirement sums?

To maximize your CPF retirement savings, consider contributing more to your CPF account to meet the updated retirement sums. Explore different CPF LIFE options and make voluntary contributions, especially if you are self-employed, to increase your retirement income.

What changes have been made to the CPF withdrawal policies for retirees?

The CPF withdrawal policies have been updated to ensure that individuals aged 55 and older have their funds automatically transferred into their Retirement Account (RA) to meet the Full Retirement Sum (FRS) limit. This change ensures adequate savings for long-term financial security.

What is the importance of the Enhanced Retirement Sum (ERS) in CPF retirement planning?

The Enhanced Retirement Sum (ERS) is crucial in CPF retirement planning as it provides the highest monthly payouts under the CPF LIFE scheme. This tier is designed for those wishing to maximize their retirement income, thereby ensuring greater financial stability.

How often will the CPF retirement sums be reviewed and updated?

The CPF retirement sums are reviewed annually to ensure they align with inflation and the rising cost of living. This regular review helps maintain the financial security of retirees and adapts to changing economic conditions.

What proactive steps can I take to prepare for CPF retirement planning changes?

To prepare for CPF retirement planning changes, maximize your contributions, explore different CPF LIFE payout plans, make voluntary contributions if self-employed, and stay informed about CPF updates through seminars and workshops.

How do I calculate my expected monthly payouts under the new CPF retirement sums?

Your expected monthly payouts under the new CPF retirement sums can be calculated based on the tier you choose—BRS, FRS, or ERS. The CPF website provides a calculator to help estimate your monthly payouts based on your contributions and the selected retirement sum.

| Retirement Tier | Sum in 2023 | Sum in 2024 | Monthly Payout in 2024 |

|---|---|---|---|

| Basic Retirement Sum (BRS) | SGD 96,000 | SGD 105,000 | SGD 900–1,000 |

| Full Retirement Sum (FRS) | SGD 192,000 | SGD 210,000 | SGD 1,800–2,000 |

| Enhanced Retirement Sum (ERS) | SGD 288,000 | SGD 315,000 | SGD 2,600–2,800 |

Summary

CPF retirement planning is crucial for ensuring a secure financial future in Singapore. The recent updates to the CPF system, including increased retirement sums and the introduction of benefits for self-employed workers, are designed to enhance the financial stability of retirees. By understanding the new tiers and taking proactive steps to maximize contributions, Singaporeans can better prepare for retirement and enjoy their golden years with peace of mind.