CPF retirement planning is an essential aspect of securing your financial future in Singapore. The Central Provident Fund (CPF) serves as the backbone of retirement funds in the country, ensuring that individuals have sufficient savings to support themselves during their golden years. With recent CPF changes in 2024, including updates to retirement sum tiers, it’s crucial for Singaporeans to understand how these adjustments can impact their retirement payouts. These tiers, which include the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS), directly influence the monthly CPF LIFE payouts that retirees can expect. As living costs continue to rise, effective CPF retirement planning becomes more important than ever to ensure long-term financial stability.

When discussing retirement savings strategies in Singapore, it’s essential to consider the role of the Central Provident Fund (CPF) in providing financial security for future retirees. The CPF system has undergone significant revisions recently, particularly with the introduction of new retirement sum tiers aimed at enhancing monthly payouts for individuals. Updates to CPF policies, especially concerning self-employed CPF benefits, reflect a growing recognition of the diverse workforce in Singapore. By understanding these changes and their implications, individuals can better prepare for a comfortable retirement and take full advantage of the CPF LIFE annuity scheme. As the landscape of Singapore’s retirement funds evolves, staying informed is key to making the most of available resources.

Understanding CPF Retirement Planning

CPF retirement planning is essential for Singaporeans aiming for financial security in their golden years. The Central Provident Fund (CPF) serves as the backbone of retirement savings, allowing individuals to accumulate funds through mandatory contributions from both employers and employees. This model not only supports retirement but also healthcare, housing, and education needs. Understanding how to effectively utilize CPF accounts is paramount for ensuring a stable income post-retirement.

The CPF system is structured around various accounts, including the Ordinary Account, Special Account, and MediSave Account, each serving distinct purposes. The retirement savings accumulated in these accounts can be strategically managed to maximize benefits during retirement. For instance, retirees can choose their preferred CPF LIFE scheme, which determines their monthly payouts based on the amount saved. By aligning savings strategies with the CPF retirement sum tiers, individuals can better prepare for their financial future.

Key Changes to CPF Retirement Sums in 2024

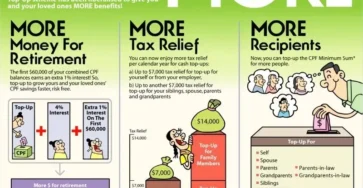

In 2024, significant changes to the CPF retirement sums will take effect, impacting how much Singaporeans need to save for their retirement. The government has announced increases across the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS), ensuring that monthly payouts align with rising living costs. For example, the BRS will increase from SGD 96,000 to SGD 105,000, translating to higher monthly payouts of between SGD 900 and SGD 1,000.

These adjustments underscore a proactive approach to retirement planning, as individuals must now reassess their savings strategies to meet these new requirements. The increased sums aim to provide greater financial security, allowing retirees to cover essential expenses comfortably. As such, understanding the nuances of these changes is crucial for effective CPF retirement planning.

Exploring the Retirement Sum Tiers

The CPF retirement sum tiers—BRS, FRS, and ERS—play a pivotal role in determining the financial stability of retirees. The BRS provides a basic safety net for individuals with additional income sources, while the FRS offers a more secure option for those relying primarily on CPF savings. The ERS is ideal for those aiming for a luxurious lifestyle, providing the highest monthly payouts. By choosing the appropriate retirement sum tier, individuals can customize their retirement plans based on their financial goals.

Each tier comes with distinct monthly payout ranges that cater to different retirement lifestyles. For example, the FRS, which increases to SGD 210,000 in 2024, ensures that retirees can manage additional costs like healthcare and housing. Understanding these options allows individuals to make informed decisions about their CPF accounts and how they will support their retirement lifestyle.

Self-Employed CPF Benefits in 2024

For self-employed workers, 2024 brings promising updates to CPF benefits, enhancing their access to financial security during retirement. New policies will allow self-employed individuals to receive monthly payouts ranging from SGD 200 to SGD 400 based on their contributions. This marks a significant shift in how self-employed individuals can prepare for retirement, ensuring they are not left behind in the CPF system.

Moreover, self-employed workers are encouraged to make voluntary contributions to their CPF accounts, which can be allocated to Ordinary, MediSave, and Special Accounts. This flexibility aims to bolster their retirement savings and ensure they can enjoy a comfortable lifestyle post-retirement. As these benefits expand, it is essential for self-employed individuals to familiarize themselves with the CPF system and integrate these contributions into their overall retirement planning.

Projected Increases for Enhanced Retirement Sum

The Enhanced Retirement Sum (ERS) is set for significant growth, reflecting the government’s commitment to ensuring retirees receive adequate financial support. Projections indicate that the ERS cap will rise from SGD 288,000 in 2023 to SGD 315,000 in 2024, with expected monthly payouts reaching SGD 2,600 to SGD 2,800. This increase is designed to provide the highest level of financial stability for retirees who wish to maximize their monthly income.

As the ERS continues to rise, individuals planning for retirement should consider how this affects their savings strategies. With higher caps on retirement sums, there is an opportunity for retirees to enjoy a more comfortable lifestyle. Individuals should regularly assess their financial situation and explore options to contribute towards the ERS, ensuring they can benefit from these enhanced payouts in the future.

Impact of Changes to Retirement Age

The gradual increase in the retirement age in Singapore is a crucial factor in retirement planning. Starting in 2024, the retirement age will remain at 63, with a planned rise to 64 in 2026 and 65 by 2030. This incremental approach gives individuals more time to save for retirement, allowing them to build a more substantial CPF account balance. As life expectancy increases, this adjustment helps ensure that individuals can work longer while preparing for a financially secure retirement.

By extending the working age, the government aims to help individuals amass greater savings in their CPF accounts, which translates into higher monthly payouts upon retirement. This change encourages proactive planning, as workers should take advantage of additional working years to enhance their retirement funds. It is essential for individuals to stay informed about these changes and strategize accordingly to maximize their CPF benefits.

Revised Withdrawal and Transfer Policies for CPF

Recent updates to the withdrawal and transfer policies within the CPF system are designed to enhance efficiency and provide better benefits for retirees. Individuals aged 55 and above will see their funds from the Ordinary Account and Special Account automatically transferred into the Retirement Account (RA) to meet the Full Retirement Sum (FRS) limit. This ensures retirees have adequate savings allocated for long-term financial security.

Additionally, remaining funds in the Ordinary Account that exceed the FRS will be retrievable at any time, granting retirees immediate access to additional cash if needed. Starting in 2025, the merging of the Special Account into the Retirement Account will optimize interest rates for retirement-focused savings, enhancing overall financial growth. Understanding these revised policies is crucial for retirees to manage their funds effectively.

Preparing for Retirement with CPF

To maximize the benefits of the CPF system, individuals should adopt proactive measures in their retirement planning. One of the most effective strategies is to maximize CPF contributions, ensuring that individuals meet or exceed the new retirement sums. This proactive approach will lead to higher monthly payouts during retirement, providing greater financial security.

Additionally, exploring different CPF LIFE options is vital for retirees to select the plan that best suits their financial needs. For self-employed individuals, making voluntary contributions can significantly boost retirement savings, enabling a more comfortable retirement lifestyle. Staying informed about CPF updates and participating in seminars can also empower individuals to make informed decisions regarding their retirement planning.

The Importance of Staying Informed About CPF Changes

Staying informed about changes to the CPF system is crucial for effective retirement planning. With updates such as increased retirement sums and changes to withdrawal policies, understanding how these alterations impact individual savings strategies can greatly influence financial outcomes. Regularly checking CPF announcements, attending workshops, and engaging with financial advisors can help individuals navigate the complexities of the CPF system.

Moreover, being aware of how these changes align with personal financial goals allows for more strategic planning. For instance, individuals can assess their current savings and adjust their contributions accordingly to meet the new retirement sum tiers. By prioritizing education around CPF and its benefits, Singaporeans can enhance their retirement preparedness and ensure a secure financial future.

Frequently Asked Questions

What are the main changes to CPF retirement planning in 2024?

In 2024, significant changes to CPF retirement planning include increases in the retirement sum tiers: Basic Retirement Sum (BRS) will rise to SGD 105,000, Full Retirement Sum (FRS) to SGD 210,000, and Enhanced Retirement Sum (ERS) to SGD 315,000. These adjustments aim to provide higher monthly payouts during retirement, ensuring financial stability for retirees.

How do the retirement sum tiers affect CPF retirement planning?

The retirement sum tiers—Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS)—determine the monthly payouts retirees receive from CPF LIFE. Effective planning requires understanding these tiers, as higher sums correlate with greater financial security during retirement.

What are the self-employed CPF benefits introduced in 2024?

In 2024, self-employed individuals can benefit from CPF retirement planning through new policies that allow for monthly payouts ranging from SGD 200 to SGD 400, dependent on contributions. This inclusion ensures that self-employed workers can also secure their retirement through CPF.

How can I maximize my CPF LIFE payouts for retirement?

To maximize your CPF LIFE payouts, consider contributing more to reach the higher retirement sum tiers, choosing the appropriate CPF LIFE plan (Standard, Escalating, or Basic), and making voluntary contributions if you’re self-employed. Understanding these aspects of CPF retirement planning will enhance your financial security in retirement.

What is the impact of the retirement age changes on CPF retirement planning?

The gradual increase in retirement age, set to rise from 63 to 65 by 2030, allows individuals to work longer, contributing more to their CPF accounts. This change strengthens CPF retirement planning by enabling future retirees to accumulate larger savings for a more secure retirement.

What should Singaporeans do to prepare for CPF retirement planning changes?

Singaporeans should actively prepare for CPF retirement planning changes by maximizing their contributions to meet new retirement sums, exploring different CPF LIFE options, making voluntary contributions (especially if self-employed), and staying informed about CPF updates and workshops.

How do CPF retirement sums influence monthly payouts?

CPF retirement sums directly influence the monthly payouts retirees receive. For instance, meeting the Basic Retirement Sum (BRS) may yield monthly payouts of SGD 900 to SGD 1,000, while the Full Retirement Sum (FRS) offers SGD 1,800 to SGD 2,000. Effective CPF retirement planning ensures that individuals can secure adequate income during retirement.

What are the projected future changes to CPF retirement sums?

The CPF retirement sums are projected to continue increasing annually, with the BRS expected to reach SGD 110,200 by 2026 and SGD 114,100 by 2027. These changes are part of ongoing efforts to keep CPF retirement planning aligned with rising living costs, ensuring retirees have sufficient funds.

What is CPF LIFE and how does it relate to retirement planning in Singapore?

CPF LIFE is an annuity scheme that provides monthly payouts for life to retirees based on the amount accumulated in their CPF accounts. Understanding CPF LIFE is crucial for retirement planning in Singapore as it ensures a steady income stream, which is vital for financial security during retirement.

How do revised withdrawal policies affect CPF retirement planning?

Revised withdrawal policies streamline the transfer of funds from the Ordinary and Special Accounts into the Retirement Account (RA), ensuring that retirees have sufficient savings to meet the Full Retirement Sum (FRS). This efficiency enhances CPF retirement planning by ensuring retirees can access their funds when needed.

| Key Point | Details |

|---|---|

| CPF Role in Retirement | The CPF is a compulsory savings model in Singapore that provides financial support for retirees. |

| Retirement Sum Tiers | The three tiers are Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS), each offering different monthly payouts. |

| Changes in 2024 | Retirement sums will increase to help retirees cover rising living costs and longer life expectancy. |

| New Benefits for Self-Employed Workers | Self-employed individuals can now access CPF benefits and receive monthly payouts based on contributions. |

| Gradual Increase in Retirement Age | The minimum retirement age will rise from 63 to 65 by 2030, allowing more time to accumulate savings. |

| Withdrawal Policy Changes | Funds will be automatically transferred to the Retirement Account for those 55 and older to ensure adequate retirement savings. |

Summary

CPF retirement planning is crucial for ensuring a secure financial future in Singapore. With the recent updates to the CPF system, including increased retirement sums and benefits for self-employed workers, individuals have greater opportunities to enhance their savings. By understanding the new tiers and making informed contributions, Singaporeans can better prepare for a comfortable retirement.